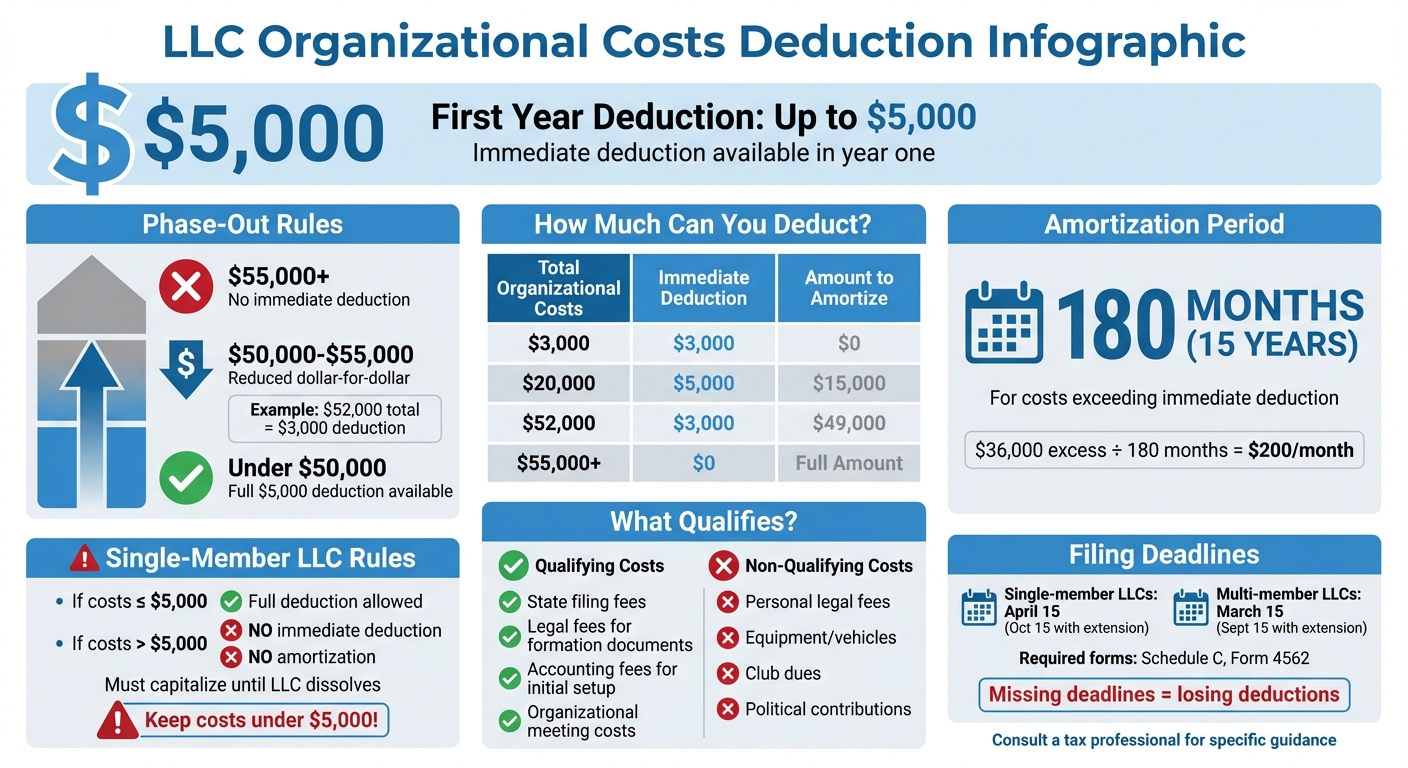

When forming an LLC, you can deduct up to $5,000 in organizational costs during your first year. These costs include legal fees, state filing charges, and accounting services directly tied to setting up the LLC. If your total expenses exceed $5,000, the remaining amount must be amortized over 180 months (15 years). However, if your total costs exceed $50,000, the $5,000 deduction is reduced dollar-for-dollar, and deductions are entirely phased out at $55,000 or more.

For single-member LLCs, the rules are stricter. If organizational costs go over $5,000, you cannot amortize the excess. Instead, the entire amount must be capitalized and only deducted upon dissolving the LLC. To maximize deductions, ensure expenses are properly tracked and categorized, and file the required tax forms (e.g., Schedule C for single-member LLCs or Form 4562 for amortization). Missing deadlines could result in losing these deductions.

Key points:

LLC Organizational Costs Deduction Guide: Limits and Rules

Organizational costs are the expenses tied directly to the legal formation of your LLC. These include fees for paperwork and professional services. It's important to distinguish these from startup tax deductions, which cover activities like market research, pre-opening advertising, and employee training. Understanding the difference helps ensure proper expense allocation.

"Organizational expenditures are costs incurred to legally form your LLC... Startup expenses are not organizational costs." – Michael D. Koppel, CPA

Keep in mind that organizational and startup costs are subject to different deduction limits and amortization rules.

Certain expenses qualify as organizational costs, such as:

These costs must be directly related to forming your LLC. To avoid confusion, request itemized bills from professionals like attorneys or accountants to separate organizational work from other services.

Not all expenses fall under the category of organizational costs. The following are excluded:

For single-member LLCs, if your organizational costs exceed $5,000, the entire amount must be capitalized instead of deducted.

When it comes to deducting organizational costs, the IRS provides clear guidelines on how and when these expenses can be claimed. LLCs are allowed to deduct up to $5,000 immediately, with any additional costs being amortized over time.

In their first year, LLCs can deduct up to $5,000 of qualifying organizational expenses right away. These expenses might include state filing fees or legal costs for preparing an operating agreement.

However, there’s a catch: if total organizational costs exceed $50,000, the $5,000 deduction is reduced dollar-for-dollar by the amount over $50,000. For instance, if your expenses total $52,000, your immediate deduction drops to $3,000 ($5,000 minus the $2,000 excess). And if your costs hit $55,000 or more, the immediate deduction is completely phased out.

"The corporation shall be allowed a deduction for the taxable year in which the corporation begins business in an amount equal to the lesser of - (A) the amount of organizational expenditures... or (B) $5,000, reduced (but not below zero) by the amount by which such organizational expenditures exceed $50,000." – 26 U.S. Code § 248

| Organizational Costs | Immediate Deduction | Amount to Amortize |

|---|---|---|

| $3,000 | $3,000 | $0 |

| $20,000 | $5,000 | $15,000 |

| $52,000 | $3,000 | $49,000 |

| $55,000+ | $0 | Full Amount |

For any organizational expenses above the immediate deduction limit, the IRS requires these costs to be amortized evenly over 180 months (15 years). The clock starts ticking in the month your business officially begins operations - not when you file your formation documents, but when you start conducting business activities.

Here’s an example: if your total costs amount to $41,000, you can deduct $5,000 immediately and then amortize the remaining $36,000 over 15 years. That works out to about $200 per month. To take advantage of this, you’ll need to elect these deductions when filing your tax return, including any extensions.

Up next, we’ll cover how to accurately report these deductions on your tax return.

Single-member LLCs operate under tighter rules compared to multi-member LLCs when it comes to deducting organizational costs. The IRS classifies single-member LLCs as "disregarded entities", meaning they are taxed like sole proprietorships unless you choose to be taxed as a corporation. This classification imposes a strict limit on what you can deduct for organizational expenses.

If your total organizational costs are $5,000 or less, you can deduct the entire amount in your first year of business. But if your costs exceed $5,000, you lose the option for an immediate deduction. Instead, all expenses must be capitalized, and you can only recover them as a loss when you dissolve the LLC.

"The moral is that if you form a one-member LLC, you should never spend more than $5,000 in organizational expenses." – Stephen Fishman, J.D., Author

To stay within these limits, keep detailed, itemized invoices that separate organizational costs from operational expenses.

It’s also important to note the difference between organizational costs and startup costs. While organizational costs face the $5,000 cap, startup costs - like market research or travel for setting up the business - are treated differently under Section 195. Even for single-member LLCs, you can deduct $5,000 of startup costs and amortize any remaining amount over 180 months, the same as other business structures.

Understanding these rules helps ensure proper tax reporting and avoids surprises down the line.

For single-member LLCs, precise reporting is critical. Organizational cost deductions should be reported on Schedule C of Form 1040. Typically, the first-year deduction is listed in Part V under "Other Expenses." If you’re also amortizing startup costs, you’ll need to complete Form 4562 (Depreciation and Amortization), specifically Part VI, for the first year. Afterward, carry the amortized amount to the "Other Expenses" section of Schedule C.

To claim your deduction, you need to file your tax return on time and include the necessary documentation. The IRS considers your election effective as long as you meet the deadline, so there's no need to file a separate election form - claiming the deduction on your return is enough.

For single-member LLCs, you must file by April 15 (or October 15 if you've requested an extension). For multi-member LLCs, the filing deadline is March 15 (or September 15 with an extension). Missing these deadlines means you lose the ability to claim the deduction.

If you're amortizing expenses, you'll need to include a statement with Form 4562. This statement should outline the costs incurred, the date your business became operational, the total organizational expenditures, and the requested amortization period.

Now, let’s look at the specific forms and deadlines based on your LLC's tax classification.

The forms you use depend on how your LLC is classified for tax purposes:

For all these classifications, Form 4562 is used to report amortization. Be sure to track and account for startup costs by keeping receipts, invoices, and any other documentation to verify your expenses and confirm when your business officially began operations.

The IRS has strict guidelines when it comes to classifying expenses, and even a small misstep can lead to missed deductions or heightened scrutiny. With the rules for organizational deductions being particularly intricate, seeking professional assistance can make all the difference.

Experienced professionals can help you navigate the distinctions between organizational, startup, and operational expenses while staying within the $5,000 deduction limit and managing the $50,000 phase-out threshold. For single-member LLCs, as mentioned earlier, this rule operates on an "all-or-nothing" basis, making careful planning essential.

Afino offers bookkeeping and corporate tax services that ensure proper documentation is maintained and Form 4562 is prepared accurately, keeping you aligned with IRS deadlines.

For a more strategic approach, CFO-level guidance can help fine-tune the timing of your business operations and develop effective cost capitalization strategies.

Beyond expert advice, maintaining a clear separation between personal and business finances is critical. Open a dedicated business account and use reliable accounting software to track expenses in real time. If you anticipate organizational costs exceeding the allowable thresholds, it's wise to consult a professional before the end of your first tax year.

This summary highlights the key takeaways from the discussion above.

Organizational cost deductions can significantly reduce your LLC's taxable income. LLCs are allowed to deduct up to $5,000 of organizational costs immediately, with any remaining amount amortized over 180 months. For single-member LLCs, expenses exceeding $5,000 must be capitalized until the LLC dissolves.

To avoid potential issues with the IRS, keep detailed and digitized records, including receipts, invoices, and clearly labeled expense descriptions. Make sure to elect to amortize these costs during your first active tax year. It’s also a good idea to consult with a tax professional to verify qualifying expenses and establish proper commencement dates before the end of the tax year.

If your LLC's organizational costs go over $55,000, you won’t be eligible for the initial $5,000 immediate deduction. Instead, you’ll need to amortize the entire amount over 180 months (15 years). This means you’ll spread the deduction out evenly over that period, gradually recouping the expenses.

This approach helps ensure that larger startup costs are deducted in a consistent and structured manner, aligning with IRS requirements.

If a single-member LLC incurs organizational costs that go over $5,000, it can still deduct up to $5,000 in the first year. The remaining amount - anything above this threshold - can be spread out and deducted over 15 years (180 months). This method aligns with IRS rules for handling start-up and organizational expenses.

By amortizing the excess costs, single-member LLCs can manage their tax deductions more effectively while staying within the guidelines. For personalized advice and accurate planning, it’s a good idea to consult a professional service like Afino.

When forming an LLC, it's essential to distinguish between organizational costs and startup costs, as they serve different purposes and are treated differently for tax purposes.

Organizational costs are the expenses directly tied to establishing your LLC. These include things like legal fees, accounting services, and state filing fees - essentially, anything directly related to creating the business entity itself.

Startup costs, however, cover the expenses you incur before your LLC is ready to begin operations. This might include market research, advertising campaigns, employee training sessions, or other activities necessary to get your business off the ground.

The IRS categorizes and handles these costs differently when it comes to deductions. To ensure you're taking full advantage of available deductions while remaining compliant, it's a good idea to consult with a financial professional.

.svg)

.svg)

.png)

.png)