Staying on top of taxes is critical for running a small business. Missing deadlines, underpaying, or failing to keep proper records can lead to penalties, interest, or even personal liability. Here's what you need to know to stay compliant:

This guide outlines deadlines, requirements by business structure, deductions, and tools to simplify compliance. Proper planning and record-keeping can help you avoid penalties and maintain your business's financial health.

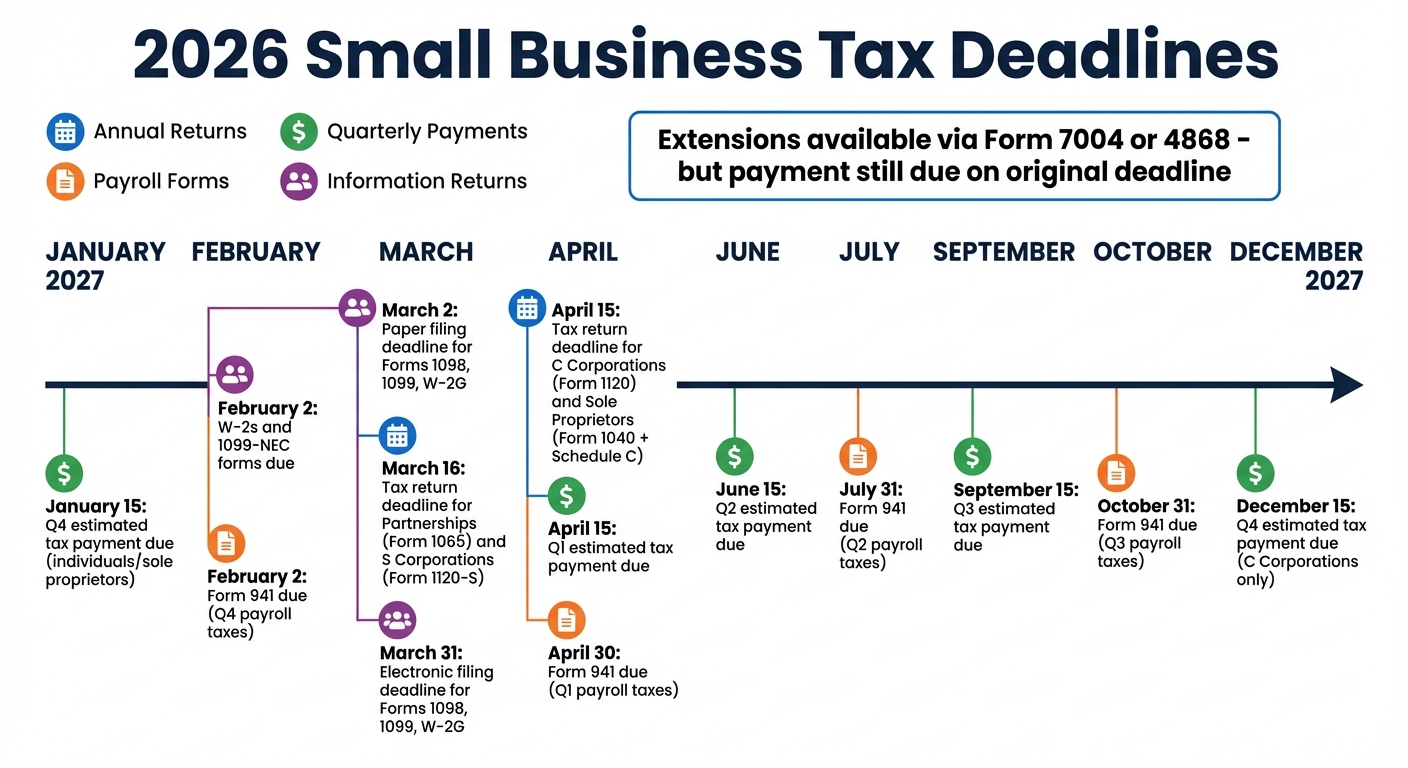

2026 Small Business Tax Deadlines Calendar

When it comes to tax deadlines, your business structure determines when you need to file. Partnerships and S corporations must submit their returns by March 16 (since March 15 falls on a Sunday) using Form 1065 or Form 1120-S. Meanwhile, C corporations and sole proprietors have until April 15 to file Form 1120 or Form 1040 with Schedule C.

Before tackling those returns, don’t forget to file information returns like W-2s and 1099-NEC forms by February 2 (observed). For other forms, deadlines vary depending on how you file. Paper filers must submit Forms 1098, 1099, and W-2G by March 2, while electronic filers get a bit more time, with a deadline of March 31.

Throughout the year, small businesses also need to make quarterly estimated tax payments. These are due on April 15, June 15, September 15, and either December 15 for C corporations or January 15, 2027 for individuals and sole proprietors. If you have employees, you’ll also need to file Form 941 quarterly, with deadlines on April 30, July 31, October 31, and February 2 for the fourth quarter of the prior year.

If you need more time to file, you can request an extension using Form 7004 or 4868. However, keep in mind that an extension only delays the filing of your return - not the payment. You’ll still need to estimate your tax liability and pay it by the original deadline to avoid penalties and interest.

Understanding and meeting these deadlines is essential. Missing them can lead to costly consequences.

Failing to meet tax deadlines can get expensive quickly. The failure-to-file penalty is 5% of unpaid taxes per month, capped at 25%. The failure-to-pay penalty, meanwhile, is 0.5% per month, also maxing out at 25%. If both penalties apply, the failure-to-file penalty is reduced by 0.5% for that month, but the combined total still hits 5%. On top of penalties, interest accrues daily on any unpaid balance at the federal short-term rate plus 3%.

For partnerships and S corporations, the stakes are even higher. The late filing penalty is $220 per owner or shareholder for each month the return is late, regardless of whether taxes are owed. Information returns like 1099s come with their own penalties - $60 per form if filed within 30 days late, escalating to $630 per form for intentional disregard.

To minimize these costs, always file your return on time, even if you can’t pay the full amount. This helps you avoid the more severe failure-to-file penalties. Pay as much as you can to reduce interest charges, and if you have a valid reason - like a natural disaster or a serious illness - you can request a penalty waiver. For added convenience, consider setting up automatic payments through the Electronic Federal Tax Payment System (EFTPS). Just make sure to schedule payments by 8 p.m. ET at least one business day before they’re due.

Your business structure plays a big role in determining how you handle tax filings. It dictates the forms you need and how payments are made.

Sole proprietorships are as straightforward as it gets - there’s no separation between the owner and the business. You’ll report your income and expenses using Schedule C and file Schedule SE if your net earnings are $400 or more.

For single-member LLCs, the IRS treats them as "disregarded entities" by default, meaning you also report activities on your personal Form 1040, using Schedule C. However, you can opt for corporate tax treatment by filing Form 8832. One key perk of an LLC over a sole proprietorship? It offers legal liability protection, keeping your personal assets safer from business debts.

Another thing to keep in mind: for 2026, the maximum net self-employment earnings subject to Social Security tax is $176,100. If you anticipate owing $1,000 or more in taxes when filing, you’re required to make quarterly estimated tax payments. Also, if you and your spouse jointly own an unincorporated business, you can elect Qualified Joint Venture status. This allows each spouse to file a separate Schedule C, avoiding the need to file as a partnership.

Next, let’s look at how partnerships and S corporations handle taxes.

Partnerships don’t pay income taxes directly. Instead, they file Form 1065, which is an informational return summarizing income, deductions, and other financial details. The IRS explains it like this:

A partnership must file an annual information return to report the income, deductions, gains, losses, etc., from its operations, but it does not pay income tax. Instead, it 'passes through' any profits or losses to its partners.

Each partner gets a Schedule K-1, detailing their share of the partnership’s income or loss. This information is then reported on Schedule E of their personal Form 1040. Additionally, partners are responsible for self-employment tax on their share of the income, which they report on Schedule SE.

S corporations work similarly in that they pass income and losses through to shareholders. The corporation files Form 1120-S and issues Schedule K-1s to shareholders, who then report their share of the income on Schedule E of their personal returns. However, unlike partnerships, S corporation shareholders don’t pay self-employment tax on their share of the income. That said, if a shareholder works for the company, they must be paid a reasonable salary, which is subject to payroll taxes. Shareholders should also make estimated tax payments if they expect to owe $1,000 or more.

Now, let’s dive into the tax rules for C corporations.

C corporations are treated as separate legal entities, which means they face double taxation - once at the corporate level on profits, and again at the shareholder level when those profits are distributed as dividends. The corporation files Form 1120 and pays corporate income tax on its earnings. Shareholders don’t report the corporation’s income on their personal returns unless they receive dividends or a salary. Dividends, when paid, are considered taxable income for shareholders.

Unlike pass-through entities, shareholders of C corporations can’t deduct corporate losses on their personal returns. If the corporation expects to owe $500 or more in taxes for the year, it must make estimated tax payments.

| Business Structure | Primary Tax Form | Pass-Through Entity? | Self-Employment Tax? |

|---|---|---|---|

| Sole Proprietorship | Form 1040, Schedule C | Yes | Yes (via Schedule SE) |

| Single-Member LLC | Form 1040, Schedule C | Yes (default) | Yes (via Schedule SE) |

| Partnership | Form 1065 and K-1s | Yes | Yes (for partners) |

| S Corporation | Form 1120-S and K-1s | Yes | No (on distributions only) |

| C Corporation | Form 1120 | No | N/A |

If you don’t already have an Employer Identification Number (EIN), make sure to apply for one at least four weeks before your tax return is due if applying by mail. Online applications are quicker and provide an EIN immediately. An EIN is essential for filing most business tax returns and for opening business bank accounts.

Deductions help reduce your taxable income, while credits directly lower the amount of tax you owe. Knowing which ones apply to your business can make a big difference when tax season arrives.

Small businesses can write off many everyday expenses, as long as they are both ordinary (common in your industry) and necessary (helpful for your business). To claim deductions, you need solid proof - think receipts, canceled checks, or mileage logs.

For vehicle expenses, you can either use the standard mileage rate - set at 70¢ per mile for 2025 - or track actual expenses like gas, repairs, and insurance. Keep in mind, if you opt for the standard rate, you must use it in the first year the vehicle is used for business. If you work from home, you may qualify for a home office deduction, but the space must be exclusively and regularly used for business. You can choose between tracking actual expenses or using the simplified method for this deduction.

Section 179 allows businesses to deduct the full cost of qualifying equipment in the year it's purchased, rather than spreading it out over several years. Other deductible expenses include travel (lodging and 50% of business meals), start-up costs, rent, insurance, and depreciation. Your accounting method also matters: under the cash method, expenses are deducted when paid, while under the accrual method, they’re deducted when incurred.

Tax credits are especially valuable because they reduce your tax bill dollar-for-dollar. One standout option is the Research & Development (R&D) Credit (Form 6765), which rewards businesses for innovation. For every qualified dollar spent on R&D, businesses typically earn 12 to 16 cents in federal and state credits. To qualify, the IRS requires activities to meet a "four-part test": they should aim to create or improve a product or process, be rooted in technology, address technical uncertainties, and involve experimentation.

Other useful credits include:

Tax laws change frequently, so it’s important to stay updated on what’s available.

The One Big Beautiful Bill Act (OBBBA), signed in July 2025, introduced key updates for the 2026 tax year. Businesses can now expense 100% of qualifying equipment, machinery, and certain plants in the first year of use for property placed in service after January 19, 2025. This replaces earlier bonus depreciation rules.

For R&D, the OBBBA reversed the 2022–2024 requirement to amortize domestic R&D costs over five years. Starting in 2025, businesses can immediately deduct these expenses again. Small businesses with average receipts of $31 million or less during 2022–2024 can even amend previous returns to claim immediate R&D deductions. If you still have unamortized R&D costs from 2022–2024, you can deduct the full balance in 2025 or spread it across 2025 and 2026.

Some credits, however, have expired. Clean vehicle credits like the New Clean Vehicle Credit (30D), Used Clean Vehicle Credit (25E), and Qualified Commercial Clean Vehicle Credit (45W) ended on September 30, 2025. Similarly, the Energy Efficient Home Improvement Credit (25C) and Residential Clean Energy Credit (25D) are no longer available for property placed in service after December 31, 2025.

Starting in 2026, bronze and catastrophic health insurance plans will be HSA-compatible. Individuals in direct primary care arrangements can also contribute to HSAs and use those funds tax-free for DPC fees.

Another change involves the 1099-K reporting threshold. The new rule applies backup withholding only if total payments exceed $20,000 and there are more than 200 transactions in a calendar year. This replaces the previous $600 threshold, giving small businesses more flexibility before triggering reporting requirements.

Once you’ve got a handle on tax deadlines and payment requirements, the next step is to focus on keeping detailed records. Good record-keeping not only ensures you meet IRS requirements but also makes audits less stressful and helps you stay on top of your business finances. The IRS expects you to back up all deductions, credits, and income with proper documentation, so staying organized can save you from penalties down the road.

A reliable system for tracking income and expenses is essential. This includes maintaining receipts, invoices, deposit slips, and any other supporting documents.

For income, keep items like cash register tapes, deposit slips, invoices, and Forms 1099-MISC. When it comes to expenses, hold onto canceled checks, credit card statements, invoices, and cash receipts that detail the payee, amount, proof of payment, and date.

If you own assets, document their purchase date, price, any improvements made, and deductions (like depreciation or Section 179 expenses). For employment taxes, retain records such as employee compensation details, Forms W-2 and W-4, and payroll tax deposit receipts.

Electronic accounting systems or point-of-sale (POS) software can simplify this process by recording transactions, reconciling accounts, and generating reports that meet IRS standards. Since your business checking account often serves as the main source for entries, reconciling it regularly is particularly important.

By keeping everything organized, you’ll also make it easier to decide how long to hold onto specific records.

Knowing how long to keep records is just as important as keeping them in the first place. For most tax-related documents, the standard retention period is three years from the date you file your return. However, some situations call for longer retention times:

"Well-organized records make it easier to prepare a tax return and help provide answers if your return is selected for examination or if you receive an IRS notice." - Internal Revenue Service

Using automated tools can help you stick to these timelines without much hassle.

Thanks to digital tools, staying on top of record-keeping has never been easier. Modern accounting software can handle tasks like categorizing transactions, reconciling bank accounts, and generating tax-ready reports. The trick is to choose a system that records transactions in real time and organizes documents by year and type of income or expense.

When selecting software, look for features that separate business and personal receipts, distinguish taxable income from non-taxable amounts, and track asset basis for depreciation. It should also support detailed records for specific expenses, such as travel or gifts, which often require extra documentation.

For example, Afino offers a bookkeeping service integrated with QuickBooks for $400 per month. It automates tasks like transaction recording, bank reconciliation, and real-time financial reporting. Plus, it ensures compliance with US GAAP and provides dedicated support, so you can focus on running your business without worrying about your books.

Make it a habit to record expenses as they happen. Organize receipts by category and year to avoid scrambling if the IRS ever comes knocking. Remember, the burden of proving deductions always falls on you.

Once your records are in order, the next step is managing employment taxes. These include federal withholding, FICA, FUTA, and the Additional Medicare Tax, all of which need to be handled correctly to avoid penalties.

Employment taxes cover federal income tax withholding, Social Security and Medicare taxes (FICA), and Federal Unemployment Tax (FUTA). Federal income tax is deducted from employees' wages based on the details they provide on Form W-4. For Social Security and Medicare, you deduct the employee's share from their paycheck and match that amount with your own funds.

The Additional Medicare Tax of 0.9% applies to wages exceeding $200,000 annually. Unlike regular Medicare taxes, this has no employer match, but you’re still required to withhold it. FUTA, on the other hand, is entirely your responsibility as the employer and isn't taken from employees' wages. For 2025, the Social Security wage base limit has increased to $176,100, up from $168,600 in 2024. Once an employee reaches this threshold, you no longer withhold Social Security tax for the remainder of the year.

All federal tax deposits must be made electronically through the Electronic Federal Tax Payment System (EFTPS). Quarterly reporting of these taxes is done using Form 941, while FUTA taxes are reported annually on Form 940.

Understanding these basics is essential, but year-end reporting obligations are equally important for staying compliant.

At the end of the year, you must issue Form W-2 to all employees and file a copy with the Social Security Administration. For independent contractors paid $600 or more during the year, you’ll need to issue Form 1099-NEC to report their compensation. If you issue 10 or more W-2 forms in a year, e-filing is mandatory.

Keep detailed records of wages, employee addresses, Social Security numbers, and W-4 forms for at least four years. If you’ve claimed credits like qualified sick and family leave wages or the employee retention credit, retain those records for at least six years.

Meeting these requirements is key to avoiding costly payroll errors.

Some common payroll mistakes include missing deposit deadlines, misclassifying workers, and incorrect withholding. Using EFTPS or a payroll service that automates deposits can help you avoid late penalties. Worker misclassification is another frequent issue. The IRS considers not just the results of the work but also how it’s performed. If you’re unsure, consult Publication 15-A or file Form SS-8 for an official determination.

Incorrect withholding often stems from outdated W-4 forms or using the wrong withholding tables from Publication 15-T. Encourage employees to update their W-4 whenever their financial or personal circumstances change. Additionally, monitor wage thresholds throughout the year to ensure you stop Social Security withholding once the annual limit is reached and start Additional Medicare Tax withholding when wages exceed $200,000.

Afino’s bookkeeping service, which integrates seamlessly with QuickBooks, can simplify payroll management. By automating payroll and transaction recording, along with offering real-time reporting and dedicated support, it helps catch potential issues before they turn into expensive problems.

To keep your business running smoothly and avoid penalties, it's essential to meet state and local tax obligations. These can include income taxes, sales taxes, and franchise taxes. Let’s break down how each of these impacts your business.

In 2026, the SALT deduction cap will jump from $10,000 to $40,000, which could bring some relief for businesses in high-tax states. Adjusted for inflation, the cap is projected to be around $40,400 for that year. Plus, it’s set to increase by 1% annually through 2029.

If your business operates as a pass-through entity - like an LLC, S corporation, or partnership - you might want to explore a Pass-Through Entity (PTE) tax election. This allows state income tax to be paid at the business level instead of personally. Currently, 36 states offer this option. However, certain states, including California, New Jersey, and Pennsylvania, don’t align with federal QBI rules. Before opting for a PTE election or making estimated payments, it’s wise to model outcomes at both the entity and owner levels, particularly if your business spans multiple states.

While income taxes vary by state, sales taxes bring their own set of challenges.

Sales tax is entirely managed by state and local governments. As a business, you’re responsible for collecting and remitting sales taxes on their behalf. To comply, you’ll need to register for sales tax in any state where you have a nexus. Nexus can be triggered by factors like a physical presence, employees, or reaching certain sales thresholds through online sales. Once registered, you must collect the appropriate tax rate from customers and remit it according to the state’s schedule - monthly, quarterly, or annually.

Many states make it easier by participating in the IRS e-file program, letting you file state returns electronically alongside your federal filings. Accurate record-keeping is essential here - track both gross receipts and the sales tax you collect. Keep in mind, for federal tax purposes, sales tax collected and remitted isn’t considered part of your business’s gross income.

Franchise taxes, sometimes referred to as "privilege taxes", are fees businesses pay for the right to operate in a state. Unlike income taxes, franchise taxes aren’t tied to profits - you’ll owe them even if your business operates at a loss. As of 2024, 13 states, including California, Delaware, Texas, and New York, impose franchise taxes.

These taxes vary widely. For instance, Delaware charges between $175 and $250,000, while California has a minimum fee of $800 for certain entities. Texas calculates its franchise tax using a margin formula based on total revenue, with multiple deduction options available.

"A franchise tax is levied on a business for the privilege of doing business in a state while income tax is levied on its profits." - Investopedia

Activities like selling products, hiring employees, or maintaining a physical presence in a state can trigger franchise taxes. Sole proprietorships are typically exempt since they aren’t registered as separate legal entities. Non-payment or late payment can have serious repercussions. For example, Delaware imposes a $200 penalty plus 1.5% interest per month for late payments. States may also revoke your business license, damage your credit score, or place tax liens on your assets. Some states even require filing a "zero return" if no tax is owed, just to avoid penalties or audits.

Staying on top of these obligations is crucial for keeping your business in good standing. Solid record-keeping is your best defense against errors or penalties.

Afino’s bookkeeping service can simplify this process. With real-time reporting and QuickBooks integration, you’ll have the tools and support needed to manage your state and local tax responsibilities effectively.

To keep your tax compliance on track, focus on a few key points. First, know your business structure and its specific tax obligations - whether you're a sole proprietor filing a Schedule C or a C corporation handling quarterly estimated payments. The federal tax system operates on a pay-as-you-go basis, so make those quarterly payments on time and keep a detailed record of every deduction to maintain financial stability.

Speaking of deductions, meticulous documentation is essential. Hold onto employment tax records for at least four years, and set up a system that tracks your income and expenses from the very beginning. This isn’t just about staying compliant with tax laws - it’s about gaining a clear financial picture to make informed business decisions.

Don’t overlook state and local taxes. Income tax, sales tax, and franchise taxes all play a role in your overall compliance strategy.

"You are responsible for all the information on your tax returns, no matter who prepares them." - Taxpayer Advocate Service

To make this process easier, Afino offers bookkeeping and corporate tax services designed to simplify compliance. With QuickBooks integration and real-time reporting, plus expert guidance, you can protect your business from penalties while improving tax efficiency.

Staying on top of tax deadlines is crucial for small businesses in 2026 to avoid penalties and maintain compliance. Here are some of the most important dates to mark on your calendar:

Depending on your business structure and specific filing requirements, there might be additional deadlines to consider. Staying organized is key - using reliable tax software or working with a tax professional can help ensure you meet these obligations on time.

To stay on top of tax requirements, small businesses need to keep financial records that are both organized and detailed. This means tracking everything - income, expenses, receipts, invoices, and payments. Using consistent categories and regularly comparing your records to bank statements can help you catch and fix errors before they become bigger problems.

Whether you choose accounting software or prefer traditional physical ledgers, having a system in place makes record-keeping much easier and more accurate. Keeping your records up to date not only simplifies tax filing but also provides a clear audit trail if the IRS ever comes knocking. If you’re unsure about what’s required, consulting a professional - like an accountant or bookkeeper - can ensure your records meet legal standards and reduce the chances of penalties or audits.

Good record-keeping isn’t just about compliance - it’s also key to hitting tax deadlines, claiming deductions you’re entitled to, and avoiding common mistakes. Make it a regular habit to review and update your records so you can stay in control of your business’s financial health.

Small businesses have several tax deductions and credits at their disposal to help reduce taxable income and ease their overall tax burden. Common deductions cover everyday business expenses like supplies, equipment, rent, utilities, and other necessary costs. If you operate from home, you might qualify for a home office deduction, and expenses tied to business-related vehicle use are often deductible too.

Tax credits can also lead to meaningful savings. For instance, the Small Business Health Care Tax Credit helps offset the cost of providing employee health insurance, while the Work Opportunity Tax Credit rewards businesses for hiring individuals from specific targeted groups. Don’t overlook asset depreciation either - it’s another key deduction that can make a difference.

To get the most out of these opportunities and stay compliant, maintaining detailed, accurate records of all expenses and transactions is crucial. These deductions and credits are designed to ease costs and support small business growth, making them an essential part of smart tax planning.

.svg)

.svg)

.png)